This sample Latin America’s Trade Performance Research Paper is published for educational and informational purposes only. Like other free research paper examples, it is not a custom research paper. If you need help writing your assignment, please use our custom writing services and buy a paper on any of the economics research paper topics.

Latin America has witnessed impressive economic growth since 2003. The average annual growth of the gross domestic product (GDP) for Latin America has been 5% for the 2003-2007 period, the highest in three decades. Trade performance has been one of the essential factors in explaining this growth. The purpose of this article is to analyze the main elements of Latin America’s trade performance from the 1990s until recent years and to explain whether global demand and economic reforms of the 1990s helped strengthen the role of the region’s trade sector.

Latin American countries have had both a positive and negative relationship with the global economy. After their independence around the beginning of the nineteenth century, most of them were involved in the first period of globalization. During this first era of globalization, Latin America based its economic growth on trade of basic commodities with Europe (for some countries, exports represented more than 60% of GDP). With World War I and the Great Depression, international prices of commodities fell, affecting the Latin American countries. An inward-looking economic model known as import substitution industrialization (ISI) was pursued to eliminate industry’s growing dependence on imports and the negative impacts of external shocks from the global economy. Although ISI was crucial in the construction of a manufacturing industry for countries such as Mexico, Brazil, and Argentina, there were also inconsistencies in industrial and trade policies. In the end, this had consequences for the whole economy. After three decades of ISI, it was clear for Latin American governments that it was not possible to uphold an industry based on a growing demand for imported inputs relying on foreign debt.

Throughout the 1970s, Latin America obtained low-interest loans. However, after the oil crisis in 1973 and the economic depression through those years, real interest rates increased. As a consequence, Latin American countries entered into a decade of debt crisis. The period 1980-1989 is known as the lost decade because of Latin America’s poor economic performance, increase in poverty, and lack of viable solutions.

Latin American countries began a process of trade liberalization after several stabilization programs. The positive numbers in the trade account (exports minus imports) during the first years of the twenty-first century were the result of two factors. The first was the economic reforms whereby exports were again the growth engine during the 1990s. The second factor was the fact that the positive global economic conditions enhanced commodity prices, which made Latin America again dependent on the volatilities of the foreign market.

This second era of globalization set new challenges for Latin America. The current global economic conditions with the financial crisis will very likely slow down the region’s economic growth. However, it can be seen as a juncture to reevaluate Latin America’s trade specialization in the global economy. This change would imply diversification of export destinations, increase the participation of manufacturing products in exports, and consolidate efforts for regional economic integration.

This research paper consists of three sections: (1) trade liberalization process, which reviews the main aspects of economic reforms in the 1990s; (2) trade performance in Latin America 2000-2007, which includes analyses of statistics referring to exports and imports (since demand of exports from China has been an important element in trade performance, there is a subsection regarding the trade between Latin America and China); and (3) the financial crisis of 2008 and trade performance, which evaluates how the global economy’s slowdown would affect the region.

Trade Liberalization Process

This section covers the main elements of Latin America’s trade liberalization process that started for most countries in the 1990s. It will give a perspective on how economic reforms transformed the trade sector where exports had become the main engine of growth.

Theory

Regarding the potential benefits of trade liberalization, Krugman and Obstfeld (2000) stated that an economic opening through tariff reduction eliminates distortions for consumers and producers with the consequent increase in national welfare. An increase in competition through the supply of imported goods in the domestic market pushes prices down with direct benefits for consumers. Dornbusch (1992) pointed out that trade liberalization brings potential dynamic benefits, for example, through the introduction of a new method of production, the opening of a new market, or the carrying out of new production methods. With the same approach, Rodrik (1999) affirmed that benefits from opening markets are not on the side of exports but rather on the side of imports. According to him, developing countries can benefit from imports of capital and intermediate inputs that are too expensive to produce locally.

One of the main criticisms of free trade and its application to developing countries has been that models of free trade suppose perfect competition in the market. However, Latin America’s industries are imperfect market structures. Therefore, selective tariffs on industries can prevent additional distortions in the economy. This is referred to as the market failure justification for infant industry protection (Krugman & Obstfeld, 2000).

This argument against trade liberalization in Latin America was used to emphasize its potential negative effects on local industry. If the speed of trade liberalization were too fast (i.e., the tariff reduction is not gradual), the industry would not have time to adjust to upcoming competition after a period of high protection. The results would be the loss of jobs and wiping out of small and medium enterprises that probably could not compete with multinational corporations.

According to Ffrench-Davis (2005), the competitiveness of the industrial sector should not be based on low wages, government subsidies, or tax exemptions. Industrial policies should aim to increase productivity in the export sector. The export sector promoted by these policies should generate value added and spillovers to the rest of the economy (activities such as the maquiladoras, where the value added and spillovers are small, could not be part of these efforts).

These different points of view about benefits and cost of trade liberalization provide an introduction for Latin America’s economic policies during the 1990s.

Economic Reforms of the 1990s

Most Latin American economies used different stabilization programs as a result of the debt crisis. The decade of the 1980s was known as the lost decade because of the severe impact on GDP per capita (the average annual percentage change of real GDP per capita was -0.4% for the region), inflation (Argentina: 385% and Brazil: 228% both in 1985 or Bolivia: 2,252% for the 1980-1985 period), and the increase of poverty (39% of Latin America’s population lived in poverty in 1990 compared with 35% in 1980; Helwege, 1995). At the end of the 1980s, most of Latin America engaged in economic reforms that had exports as the main engine of economic development. A second era of globalization began with economic reforms that included privatization (reducing the role of the state in the economy) and trade liberalization (opening the economy).

These economic reforms were part of what is now termed the “Washington Consensus” reforms or the neoliberal policies (free-market approach). Williamson (1990) summarized in an article the 10 policy instruments that institutions such as the U.S. Treasury, the International Monetary Fund (IMF), the World Bank, and the Inter-American Development Bank (all of them located in Washington, D.C.) advised as the most significant economic reforms for Latin America. These were fiscal discipline, reordering public expenditure priorities, tax reform, liberalizing interest rates, a competitive exchange rate, trade liberalization, liberalization of foreign direct investment (FDI), privatization, deregulation, and property rights (Williamson, 1990).

Throughout this period, several Latin American countries entered into a period of democratic processes (e.g., elected presidents Alfonsin in Argentina, Siles in Bolivia, Collor in Brazil, and Belaunde in Peru), which helped with the implementation of these economic policies. Besides reduction of the role of the state, economic policies pursued an increase in international trade’s participation and promotion of private investment. Argentina followed closely the Washington Consensus recommendations. However, this country suffered from a peso crisis and a reduction of GDP (as a consequence, unemployment levels reached record levels of 20% in 1995; Hoftnan, 2000). Countries such as Brazil decided not to follow the neoliberal approach. It established a middle path with changes in a slow pace with different stabilization plans (heterodox reforms).

Trade Performance in Latin America 2000-2007

Main Economic and Social Characteristics

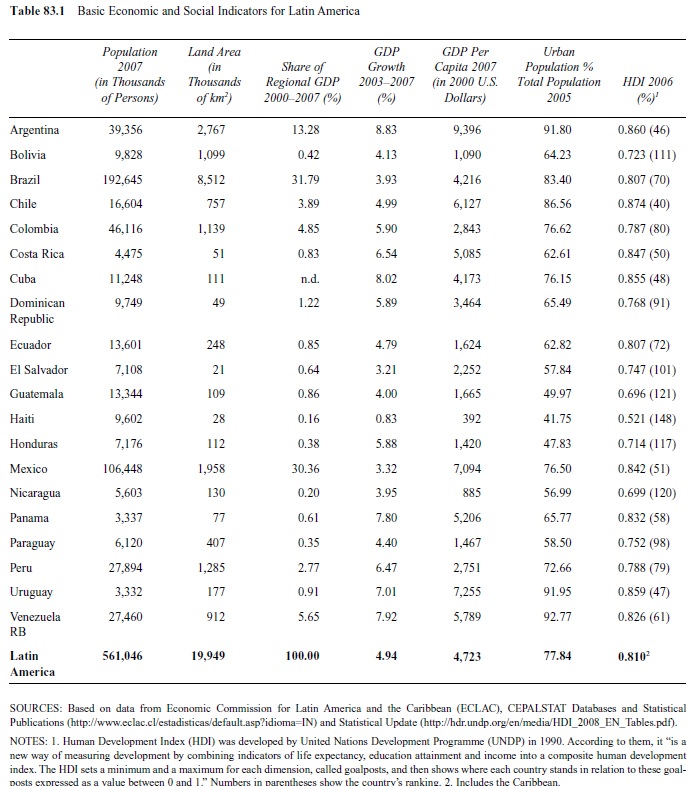

Table 83.1 summarizes the main economic and social characteristics of Latin American economies for recent years. These data offer an outlook on similarities and differences among these nations.

Generally speaking, Brazil and Mexico account for more than half of the total region’s population. Latin America’s land area is bigger than the size of the United States and Canada together. The land areas range from El Salvador with 8.1 thousand square miles to Brazil with 3.3 million square miles. Natural resources are diverse because of geographical and geological conditions. The Andes cross South America from north to south where mineral resources are relatively abundant in countries such as Chile, Peru, and Bolivia. The tropical climate of Colombia is suitable for coffee production, while the conditions of Argentina’s plains are good for the cattle industry.

Table 83.1 Basic Economic and Social Indicators for Latin America

Table 83.1 Basic Economic and Social Indicators for Latin America

As can be seen in Table 83.1, Argentina, Brazil, and Mexico together explain three quarters of Latin America’s GDP, which justifies why these economies share a central role in the region’s economic performance. One of the most notable aspects in Latin American economies has been their GDP growth for the 2003-2007 period (with the exception of Haiti with a GDP growth of less than 1%). In Table 83.1, many economies show percentages of growth above 5%, while the percentage for the 1999-2002 period was only 1%. The rapid increase in commodity prices is among the factors that explain this performance, due to an increase in demand by countries such as China and India. Although the region is not homogeneous in per capita income, Argentina and Uruguay have one of the highest levels of income per capita. Haiti is among the lowest income per capita countries in Latin America with severe poverty. Overall, Central America and the Caribbean countries have the worst poverty. This assessment turns out to be more evident with the Human Development Index (HDI) indicator proposed by the United Nations Development Programme (UNDP) in 1990. The index’s objective is to add social aspects such as life expectancy, education attainment, and income to the existing economic indicators to give a broader measure of economic development. The HDI goes from 0 to 1, and countries are ranked according to this index (UNDP, 1990). The last column of Table 83.1 includes the HDI and the country’s ranking in parentheses for 2006. According to this index, Chile, Argentina, and Uruguay have shown high levels of economic development. Even though Uruguay is a small country in comparison with the rest of the region, this country can be considered as developed in terms of its HDI. Then again, although Brazil has a big economy, its HDI was below average for the overall region. As can be inferred from Table 83.1, Latin America is not a homogeneous region in social and economic terms. The trade liberalization process initiated in the 1990s allowed these countries to participate in the global economy. However, the results from that experience have not always translated into an increase in living standards.

Tariff Reduction and Regional Trade Agreements

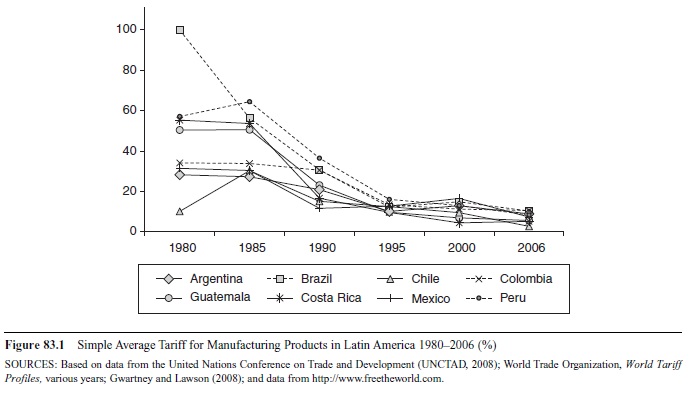

One of the policy tools used in the trade liberalization process was the reduction of tariff rates. Figure 83.1 shows Latin America’s simple average tariff for manufacturing products for the 1980-2006 period and for selected countries.

Protectionist measures taken throughout ISI led to an increase in tariff rates that lasted for several decades. In 1980, Brazil had an average tariff for manufactured imports of 99.4%, while the rest of Latin America averaged a rate of 50%. The exception was Chile since this country started opening its economy in the mid-1970s. This opening process implied for some countries joining the General Agreement on Tariffs and Trade (GATT), which in 1995 became the World Trade Organization (WTO). As members, they have to limit their tariff rates. In consequence, for 2006, the tariff rates fluctuated around 10% or less.

During the 1990s, there was a revival effort for regional economic integration as an element of trade liberalization in Latin America. The first experiences with regional trade integration occurred in the 1960s. However, attempts to form regional integration arrangements did not reach the expected results. One of the first integration experiments took place when some Central American countries (Costa Rica, El Salvador, Honduras, Nicaragua, and Guatemala) together formed the Central American Common Market (CACM) in 1960. It was created as a “custom union.” A “custom union” is a free trade area with a common external tariff for nonmembers. According to Bulmer-Thomas (2003), one of CACM’s problems was the size of its market and the inward-looking industrial policies that hurt exports of manufacturing products.

Figure 83.1 Simple Average Tariff for Manufacturing Products in Latin America 1980-2006 (%)

Figure 83.1 Simple Average Tariff for Manufacturing Products in Latin America 1980-2006 (%)

The Andean Community treaty was signed in 1969. Its objective was to build a common market between Bolivia, Colombia, Ecuador, Peru, Venezuela, and Chile. The Andean Community has been in place for four decades. It has not reached the stage of a common market. It has faced problems of coordination, and the institutions have not worked properly.

Other experiences with common markets occurred when the Caribbean countries formed the Caribbean Community and Common Market (CARICOM) in 1973, signed by all Caribbean countries. The Latin American Integration Association (LAIA) was formed in 1980 as a free trade area with most South American countries (Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, and Venezuela), as well as Cuba and Mexico.

The first regional integration agreement of the 1990s was formed with Argentina, Brazil, Paraguay, and Uruguay as members of the Southern Cone Common Market (SCCM or MERCOSUR, acronym in Spanish) in 1991.

The same year, the CACM reconstructed its trade agreement with the creation of the Central American Integration System (CAIS), adding Panama and Belize as well as one country from the Caribbean, the Dominican Republic. The Group of Three (G3) was signed by Colombia, Mexico, and Venezuela in 1995 as a free trade area. All of these regional economic integration agreements were understood as part of Latin America’s trade policy to diversify their markets and gain from specializations among the region.

Among experiences that have been successful, it is important to mention MERCOSUR. The group has expanded with the inclusion of Venezuela in 2003 and Chile as an observer member. The intra-industry trade between members has grown, particularly for Paraguay, which increased its trade from 30% in 1990 to 50% in 2005. Uruguay’s intra-industry trade increased also; more than a third of its trade is made between bloc members. However, Yeats (1997) indicated that trade barriers with third countries have affected the comparative advantages in capital goods due to high trade restriction with nonmembers of the bloc.

In addition, there have been other bilateral agreements with countries outside the region such as Mexico with the United States and Canada (North American Free Trade Agreement [NAFTA]) in 1994, Peru and the United States in 2009, or between regional groups such as MERCOSUR with the European Union (still in the process of signing an agreement).

Openness Indices

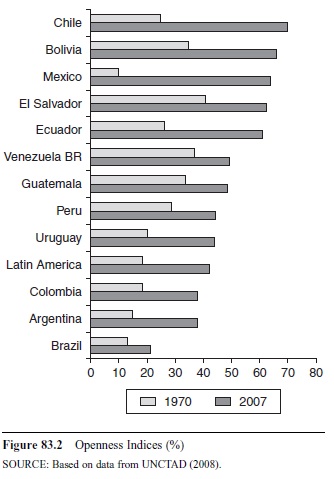

Tariff reductions and regional trade integration agreements were two significant factors for an increase in the participation of external trade (exports plus imports) as a percentage of GDP. This participation is measured as an openness index. It has been used as an indicator of the trade sector’s significance in an economy. Figure 83.2 shows the openness indices for selected Latin American countries.

Figure 83.2 Openness Indices (%) SOURCE: Based on data from UNCTAD (2008).

Figure 83.2 Openness Indices (%) SOURCE: Based on data from UNCTAD (2008).

Figure 83.2 shows the indices for 2 years, 1970 and 2007. This figure can give an overview of how extensive the external sector is now for Latin American economies. On one hand, the average share of external trade as part of GDP for the region was situated between 10% and 20% in 1970. Some small countries’ trade participation in the economy was 40% (El Salvador) or 34% (Guatemala). On the other hand, some countries moved slowly toward opening their economies. In this case, Brazil’s trade sector was 13% and Argentina’s just 14% of the GDP. Currently, Latin America is one of the most open regions in the world. As can be seen from Figure 83.2, many economies surpassed the 40% mark in 2007. In most cases, it was the increase of exports in the total trade that explained the relative performance.

Structure of Exports

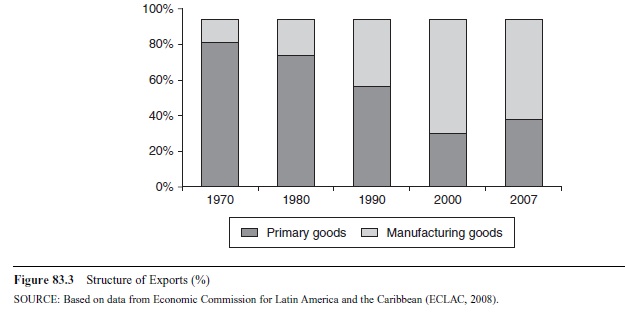

Trade liberalization had as one of its objectives the increase of manufacturing goods exports as a percentage of total trade. Figure 83.3 shows the structure of exports for Latin America for selected years.

Figure 83.3 Structure of Exports (%)

Figure 83.3 Structure of Exports (%)

This figure illustrates how until the 1980s, primary goods were the main export products. The structure of exports started to transform in the 1990s. Manufacturing goods exports were 37% for 1990 and increased to 60% in 2001. Parts and components have played a significant role in increasing manufacturing products, particularly for Brazil and Mexico, as well as exports of finished vehicles. The participation of primary goods began to intensify again in 2003 due to the rise in commodity prices (crude oil was 14.5% of total exports in 2005). In 2006, the exports of manufacturing products were just 48%.

A closer look of leading export products reveals the significance of commodities for the 1970s and the 1980s. In more recent years, there are more manufacturing products exported, particularly those from the automotive industry. The increase of manufacturing goods export has international vertical specialization as one explanation. This trade specialization began in the 1970s with multinational corporations. They established labor-intensive production stages in developing countries to reduce labor costs. The in-bond industry or maquiladora is one example of this type of manufacturing production. The maquiladora was a program initiated in 1965 in Mexico along its northern border with the United States. It was backed by a specific tariff scheme between these two countries. It allowed the imports of parts and components from the United States without duties for assembly in Mexico and subsequent export as final product for the U.S. market.

Feenstra (1998) coined the process as integration of trade and disintegration of production. As a result, there is an increase in exports of parts and components, but for countries such as Brazil and Mexico, the export of finished vehicles has become the third most important product.

Recent growth in the demand for commodity products from China and India has caused a rise in prices. On one hand, some Latin American countries (Bolivia, Chile, Peru, and Venezuela) have benefited from this important source of income. The GDP’s performance for the 2003-2007 period has as one of its determinants the increase in the demand for commodity products. On the other hand, income revenues from commodity exports have created overvalued pressures on real exchange rates. An overvalued pressure exists when the supply of foreign currency in the economy is greater than the demand. In consequence, the local currency increases in value. An overvalued exchange rate becomes an anti-export bias for noncommodities exports. In addition, inflation pressures have affected the region due in part to the commodity price boom. The average inflation rate for Latin America was 6% for the 2006-2007 period and increased to 9% in 2008. The slowdown in global economic activity due to the international financial crisis will reduce inflationary pressures. The Economic Commission for Latin America and the Caribbean (ECLAC, 2009b) predicted that Latin America’s GDP growth rate would fall off to 1.7%.

Origin and Destination of Exports and Imports

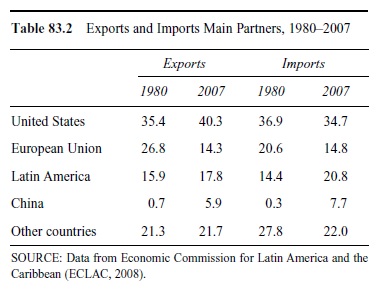

The origin and destination of exports and imports for Latin American countries can be seen in Table 83.2.

Table 83.2 Exports and Imports Main Partners, 1980-2007

Table 83.2 Exports and Imports Main Partners, 1980-2007

Table 83.2 shows the composition of exports and imports in 1980 and 2007 for trade with selected partners. Regarding exports, the U.S. market has been significant for Latin American exports. In 1980, the region sent 35% of its total exports to the United States, 27 years later increasing that percentage to 40%. The European Union market was important for some manufacturing products (automotive goods) in the 1980s but has gradually lost participation as a destination of Latin American exports (from 27% in 1980 to half of that percentage in 2007). Latin America has also been a destination for exports from members of the region. However, the composition between 1980 and 2007 has not changed significantly (16% in 1980 to 18% in 2007). China has become an important partner for some Latin American countries, particularly for the supply of commodities. Since 2003, China has become the second most important trading partner for Mexico. This performance has meant an increase in its participation as a destination market from 1%in 1980 to 6% in 2007.

The main trade partners for imports of products demanded by Latin American countries can be seen in Table 83.2. The import composition shares similarities with exports. The United States and European Union were significant as sources for imported products. Even though the participation of the European Union has decreased, there are still significant trade ties between both regions. There has been an increase in the import demand from members of the Latin American region from 14% in 1980 to 21% in 2007. Since 2003, China has increased exports to Latin America; so far, the trade balance has been positive for most Latin American countries, but the demand for Chinese products has increased steadily.

Trade With China

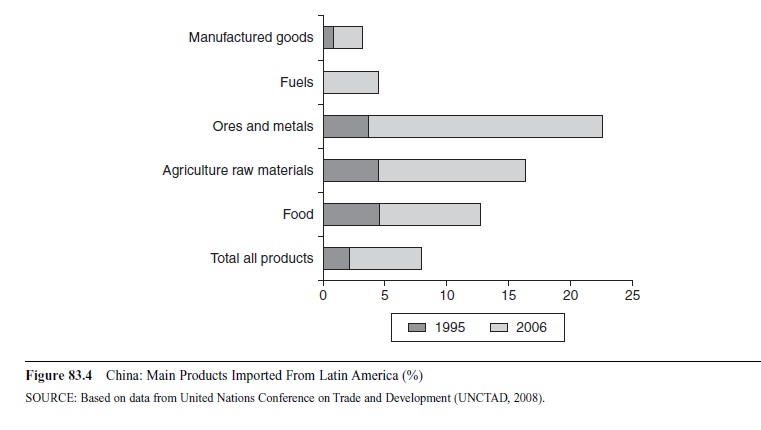

Trade with China has been an important factor for overall trade performance of Latin American economies in the past 5 years. The main goods demanded from this country are primary goods, particularly ores and metals. Figure 83.4 shows the main products imported from Latin America for 1995 and 2006. The economic growth of China since the 1980s has demanded imports of primary products for expanding its industrial base and of some agricultural products that appeal to the more sophisticated Chinese population (e.g., by-products from cattle farming).

Some Latin American countries have consolidated their trade relations with China through bilateral trade agreements. Chile was the first Latin American country to sign a free trade agreement (FTA) with China in 2005. Peru initiated negotiation toward an FTA the same year, signing an agreement in 2008. Rosales and Kuwuyama (2007) pointed out that the benefits of trading with China have been uneven for the region. South American countries have gained from an increase in terms of trade (export prices/import prices), while Central American countries have been hurt by the competition of Chinese products in the U.S. manufacturing market.

Mexico has seen its share of manufactured products decrease in the U.S. market (textiles and apparel) due to an increase in imports from China. Chiquiar, Fragoso, and Ramos-Francia (2007) calculated that Mexico lost comparative advantages (Mexican exports vs. world exports to the U.S. market) in the textile and apparel sectors because of competition by Chinese products. Even though Mexico enjoyed free-market access to the U.S. market with NAFTA, the low cost of Chinese manufacturing as well as changes in the WTO regulations explain the increase of Chinese goods in the U.S. market. Gallagher, Moreno-Brid, and Porzecanski (2008) stated that Mexico has lost competitiveness in 15 non-oil-exported products in the U.S. market due to Chinese competition. Their measurement indicates that industries that depend on unskilled labor are the most threatened.

Figure 83.4 China: Main Products Imported From Latin America (%)

Figure 83.4 China: Main Products Imported From Latin America (%)

Effects on GDP

Finally, we analyze the possible links between trade performance and its effects on GDP, employment. and industrial production. There is some argument about the positive effects of trade performance on economic growth. Empirical evidence for the 1990s has not been conclusive about this relationship (Giles & Williams, 2000). Furthermore, one of the most debated issues at that time was the slow economic growth that accompanied the posttrade liberalization period. Latin America’s per capita GDP growth rate for 1990-2004 was 0.9%, a much lower rate than the period of ISI (2.6% for 1950-1980). This rate was lower than for the East Asian countries for the 1990-2000 period (3.95%) and for the world (1.2%).

Ffrench-Davis (2005) reviewed the different approaches to explain the low economic growth of the 1990s. Some of his focus was on the stabilization programs during the 1980s and the lack of complementary reforms to support manufactured exports. For example, Dijkstra (2000) affirmed that trade liberalization effects on industrial development were mixed depending on the level of development of the industrial base in Latin American countries. He found that industrial structural changes in Chile and Brazil were explained by domestic demand and exchange rate factors rather than an increase in exports. Other studies criticized the Washington Consensus reforms and their failure to deliver the expected benefits of an open economy. This disappointment with the neoliberal economic reforms has been one of the reasons for recent trends toward more state intervention in the economy. Countries such as Venezuela, Bolivia, and Ecuador have distanced themselves from the Washington Consensus policies.

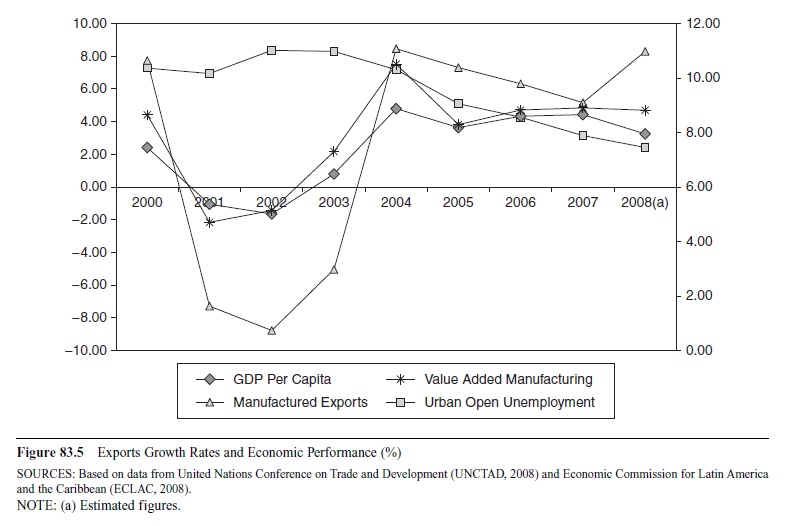

Figure 83.5 shows some indicators of growth, per capita GDP, and exports for the 2000-2008 period for Latin America.

The GDP per capita and the value-added manufacturing and total export rates of growth are depicted in the left axis, and the urban open unemployment rate is depicted in the right axis. As can be seen in the figure, the per capita GDP has grown steadily since 2003, with percentages that the region has not experienced since the ISI period (around 5%). The performance of total exports varied over this period, since between 2001 and 2003, there was a decline in the rate of growth, but it has started to increase since 2003 due to an important increase in primary product exports (more than 15% since 2004). Besides, it is important to take into consideration that during this same period, primary product exports explained more than 10% of the total GDP. As mentioned before, the international demand for these products and the favorable terms of trade have helped to shape these results. Since 2004, the value added for manufacturing products grew at rates close to 5% until 2008. One of the results of the positive performance of the economies can be seen in a reduction of unemployment. From 8% in 2000, it was reduced to close to 5% in 2008. However, the international financial crisis of 2008 affected the economic performance of the following years for the region, as we will discuss in the next section.

Figure 83.5 Exports Growth Rates and Economic Performance (%)

Figure 83.5 Exports Growth Rates and Economic Performance (%)

Financial Crisis of 2008 and Trade Performance

Latin American countries began to experience the slowdown of the global economy in 2008, particularly during the last quarter of the same year, when major problems in the U.S. financial crisis could not be solved and spread over European and Japanese financial markets. This financial crisis was a result of the real estate market’s collapse and the damage to the related financial system. The immediate consequence was a reduction in consumer spending, which brought an increase in unemployment. According to the National Bureau of Economic Research (NBER), the U.S. economy officially entered into a period of recession on December 1, 2007 (NBER, 2008).

Dealing with financial crises is not new for Latin American economies. For example, the Great Depression of the 1930s and the debt crisis of the 1980s had lasting negative consequences for many economies and took several years to stabilize. For Latin America, the main transmission channels of the global economic crisis could come from the reduction in export demand, decline in prices of commodity goods, and therefore a reduction in terms of trade as well as remittances and restrictions in financial credit sources (World Bank, 2008).

According to a number of analyses (ECLAC, 2008; International Development Bank [IDB], 2008; World Bank, 2008), most of Latin America is better prepared than before to confront external shocks due to improved management of macroeconomic policies. During the 1990s and, to a major extent, in the beginning of the twenty-first century, these countries have reduced their external debt, increased FDI flows, limited fiscal spending, and followed semi-flexible exchange rates. These macroeconomic measures should reduce the possibility of an economic crisis of big proportions. Also, the decline in foreign demand would reduce inflationary pressures that increase external demand caused during 2008 in some countries of the region such as Peru, Argentina, or Bolivia. In general terms, ECLAC (2009a) has projected a negative growth of-0.3% for Latin America and the Caribbean for 2009 and a decline of 15% in the region’s terms of trade.

The effects of the financial crisis will not be homogeneous in the region. First, it is expected that countries with commercial ties to the U.S. market will experience a sharp decline in demand for their exports. That is the case of Mexico, in which more than 60% of total exports go to the U.S. market. The Mexican economy also depends on the flow of remittances from Mexican workers living in the United States, so if those decrease, that could worsen the trade account. A reduction in remittances was expected for the rest of 2009. It could have an impact on the Mexican GDP since the remittances account for 3% of the total GDP. Moreover, ECLAC estimates a reduction of-2.0% in total GDP in 2009 (ECLAC, 2009a). The Central American countries face similar economic perspectives. The U.S. market is significant for Central America’s maquiladora products; a reduction in demand would affect these economies. Remittances also are significant for countries such as El Salvador (30% of GDP) and Honduras (20% of GDP).

The economies of South America are more diversified in terms of export destinations. Even though the U.S. market is considerable for their products, there is an important growing trade with Asian countries and intra-regional trade with countries in South America. Since the increase in demand for commodity products originates in Asian countries, particularly from China, the fall of commodity prices will have an effect on volume of exports. However, the export performance predictions for South America are not worrisome (with the exception of Argentina) since it is expected that demand of goods from countries such as China and India will continue, and these countries will maintain economic ties with South America to secure sources of primary goods for their own economic growth, although not at the same pace as during the past 5 years.

Conclusion

Trade liberalization began during the 1990s for most Latin American countries. After decades of inward-looking economic policies and the struggles to develop a strong industrial base, countries such as Brazil, Mexico, and Argentina are considered today to be emerging economies with competitive industrial sectors.

However, the economic reforms of the 1990s have proven to be a challenge for the region since the eruption of several macroeconomic collapses such as in Argentina in 2001. For that reason, there have been criticisms of the Washington Consensus approach. In fact, the discontent with the market fundamentalism of the Washington Consensus has been the reason for the conception of a new path of development in Latin America. Under a different approach, the state again is taking a role in the economy, as in Venezuela, Bolivia, and Ecuador and, to a lesser measure, in Brazil and Argentina.

In general, the first years of the twenty-first century have been relatively successful for Latin American countries. After almost two decades of stabilization programs, the region has started to experience steady economic growth from 2003 until 2007. The impact on GDP growth has been considerable, around 5% per year for the same period, a percentage that the region has not seen since three decades earlier. This performance has been explained by the rapid increase in primary goods prices. However, economic reforms from the 1990s have been a factor in the development of its external trade sector.

One of the results of trade liberalization has been a transformation in the composition of exports, with an increase of manufactured goods as a share of total exports. However, trade performance has not been homogeneous for the whole region. While Mexico’s exports are concentrated in manufactured products (including products from the maquiladora program) directed to the U.S. market, countries from South America are more diversified in terms of their export destination and share a significant intraregional trade. MERCOSUR plays an important role for the region as well as the Andean Community.

The rise of China in the global economy has been a turning point for Latin American primary goods. Since 2003, these countries have become one of the main origins of exports as well as destinations for imports coming from China. In industrial sectors such as textiles, China has been a serious competitor with Mexico and Central American countries in the U.S. market.

The financial global crisis of 2008 will have an important impact on Latin American economies. At the beginning of 2008, the economic growth rate prediction for the region was around 3%. At the beginning of 2009, that percentage was dropped to -0.1%. Latin America faces the current global financial crisis as a new test of how it can manage an external shock without entering a recession (such as in the 1930s or the 1980s). The crisis will hit countries that depend on the U.S. market for their exports more severely, such as in Mexico and Central America. Moreover, incomes from remittances also will diminish during this period. Meanwhile, South America will experience the impact of financial restrictions and the decline in the demand for primary goods. The crisis will also help countries such as Peru to cope with imminent inflation problems.

In the second era of globalization, Latin American countries are much better prepared to face external shocks. The region has stronger institutions with significant international reserves as well as fiscal and monetary discipline that will help to ease negative impacts. The financial crisis has been analyzed as evidence of market failures. For this reason, Latin America is taking this time to reassess, searching for a new path of economic development. It includes the structural economic characteristics without the need for protectionist policies or inward-looking economic policies.

The global financial crisis can be seen as an opportunity for a change in trade pattern specialization. First, a diversification of the destination of exports can reduce the dependence of demand of one country (i.e., the U.S. market). Second, increasing intra-industry trade between members of the region and efforts toward regional integration can increase the trade in manufacturing goods. Third, even though Latin American countries have a comparative advantage in primary products, there are industrial sectors that have been proven successful in the international arena, such as the automotive industry in Brazil and Mexico. Therefore, Latin America could increase the share of manufacturing products in total trade and reduce the volatilities of prices of primary goods. All of the above could result in a new role in the international economy for the region.

See also:

Bibliography:

- Balassa, B. (1971). Regional integration and trade liberalization in Latin America. Journal of Common Market Studies, 10, 58-78.

- Bulmer-Thomas, V (2003). The economic history of Latin America since independence (2nd ed.). Cambridge, UK: Cambridge University Press.

- Cardoso, E., & Helwege, A. (1997). Latin America’s economy: Diversity, trends and conflicts. Cambridge: MIT Press.

- Chiquiar, D., Fragoso, E., & Ramos-Francia, M. (2007). La ventaja comparativa y el desempeno de las exportaciones manufactureras mexicanas en el periodo 1996-2005 [Comparative advantage and the performance of the Mexican manufactured export during 1995-2005 period] (Working Paper 2007-12). Mexico DF: Banco de Mexico.

- Dijkstra, G. (2000). Trade liberalization and industrial development in Latin America. World Development, 28, 1567-1582.

- Dornbusch, R. (1992). The case for trade liberalization in developing countries. Journal of Economic Perspectives, 6, 69-85.

- Economic Commission for Latin America and the Caribbean (ECLAC). (2008). Latin America and the Caribbean in the world economy, 2007: Trends 2008. Santiago de Chile: Author.

- Economic Commission for Latin America and the Caribbean (ECLAC). (2009a, April). Economic growth in Latin America and the Caribbean will fall to -0.3% in 2009 (Press release). Santiago de Chile: Author.

- Economic Commission for Latin America and the Caribbean (ECLAC). (2009b, December). El comercio internacional en America Latina y el Caribe en 2009. Crisis y recu-peracion. Santiago de Chile: Author.

- Edwards, S. (2004). Crisis and reform in Latin America: From despair to hope. Washington, DC: World Bank.

- Feenstra, R. C. (1998). Integration of trade and disintegration of production. Journal ofEconomic Perspectives, 12(4), 31-50.

- Ffrench-Davis, R. (2005). Reforming Latin America’s economies: After market fundamentalism. New York City: Palgrave-Macmillan.

- Flam, H., & Grunwald, J. (1985). The global factory: Foreign assembly in international trade. Washington, DC: The Brookings Institution.

- Franco, P. (2007). The puzzle of Latin American economic development. Lanham, MD: Rowman & Littlefield.

- Frieden, J., Pastor, M., Jr., & Tomz, M. (Eds.). (2000). Modern political economy and Latin America: Theory and policy. Boulder, CO: Westview.

- Gallagher, K., Moreno-Brid, J. C., & Porzecanski, R. (2008). The dynamism of Mexican exports: Lost in (Chinese) translation? World Development, 36, 1365-1380.

- Giles, J., & Williams, C. (2000). Export-led growth: A survey of the empirical literature and some non-causality results. Journal of International Trade & Economic Development, 9, 261-337.

- Gwartney, J., & Lawson, R. (with Norton, S.). (2008). Economic freedom of the world: 2008 annual report. Vancouver, British Columbia, Canada: The Fraser Institute.

- Helwege, A. (1995). Poverty in Latin America: Back to the abyss? Journal of lnteramerican Studies & World Affairs, 37(3), 99-123.

- Hofman, A. (2000). The economic development of Latin America in the twentieth century. Northampton, MA: Edward Elgar.

- International Development Bank. (2008, October). The fiscal impact of the international financial crisis on Latin America and the Caribbean (Technical note). Washington, DC: Author.

- Krugman, P., & Obstfeld, M. (2000). International economics: Theory and policy (5th ed.). Reading, MA: Addison-Wesley Longman.

- Lederman, D., Olarreaga, M., & Perry, G. (Eds.). (2009). China’s and India’s challenge to Latin America: Opportunity of threat. Washington, DC: World Bank.

- Lora, E. (2001). Structural reforms in Latin America: What has been reformed and how to measure it (Research Department Working Paper Series No. 466). Washington, DC: Inter-American Development Bank.

- Lustig, N. (1994). Mexico. Hacia la Reconstruciön de una Economia [Mexico: The remaking of an economy]. Mexico DF: El Colegio de Mexico, Fondo de Cultura Econömica.

- National Bureau of Economic Research (NBER). (2008). Determination of the December 2007peak in economic activity. Cambridge, MA: Business Cycle Dating Committee, NBER.

- Rodrik, D. (1999). The new global economy and developing countries: Making openness work (Policy Essay No. 24).

- Washington, DC: Overseas Development Council. Rosales, O., & Kuwuyama, M. (2007). Latin America meets China and India: Prospects and challenges for trade and investment. Cepal Review, 93, 81-103.

- Santiso, J. E. (2007). The visible hand of China in Latin America. Paris: OECD.

- United Nations Conference on Trade and Development (UNCTAD). (2008). Handbook of statistics 2008. New York: Author. Retrieved from http://stats.unctad.org/Handbook/TableViewer/ tableView.aspx

- United Nations Development Programme (UNDP). (1990). Human development report 1990: Concept and measurement of human development, UNDP. Oxford, UK: Oxford University Press.

- Williamson, J. (1990). What Washington means by policy reform. In J. Willianson (Ed.), Latin American adjustment: How much has happened? (pp. 7-20). Washington, DC: Institute for International Economics.

- World Bank. (2008). Global economic prospects: Commodities at crossroads 2009. Washington, DC: Author.

- Yeats, A. (1997). Does Mercosur’s trade performance raise concerns about the regional trade arrangements? (World Bank Policy Research Working Paper 1729). Washington, DC: World Bank.

Free research papers are not written to satisfy your specific instructions. You can use our professional writing services to buy a custom research paper on any topic and get your high quality paper at affordable price.

ORDER HIGH QUALITY CUSTOM PAPER

Always on-time

Plagiarism-Free

100% Confidentiality

{kind=link}