This sample Tax Incidence Research Paper is published for educational and informational purposes only. If you need help writing your assignment, please use our research paper writing service and buy a paper on any topic at affordable price. Also check our tips on how to write a research paper, see the lists of research paper topics, and browse research paper examples.

The objective of tax incidence analysis is to determine who ultimately bears the burden of a tax. It is therefore an important concept for evaluating the equity of the tax system.

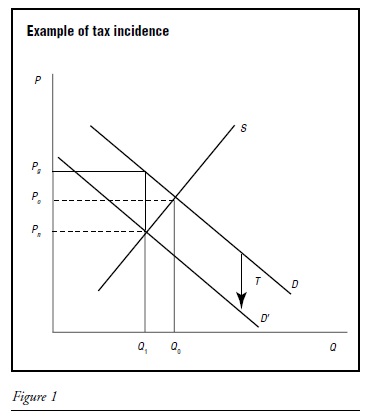

Statutory incidence assigns the burden of paying a tax to either an individual or a business, depending on the tax. However, the burden of the tax may be shifted because individuals and firms adjust their behavior when taxes are introduced or changed. As a result, economic incidence (our subject here) may differ from statutory (“legal”) incidence. A simple example is an excise tax on gasoline. As shown in Figure 1, before a tax is imposed, the equilibrium supply (S) and demand (D) is achieved at price P0 and quantity consumed of Qq. If a $1 per gallon tax is imposed, the statutory incidence is borne by the consumer when he or she pays “at the pump.” However, the consumer will not pay the full amount of the tax, because the supplier will now receive a lower after-tax price per gallon. In effect, suppliers are faced with a new demand curve, D, representing the price they will receive net of tax. This is denoted as the new demand curve, D’, in Figure 1. This demand curve is shifted down from the original demand curve, D, by $1 per unit. Per gallon of gas, the consumers now pay Pg (the gross price), producers receive Pn (the net price), and government receives P — P , or the amount of the tax (T). In the case demonstrated in Figure 1, the producer receives a lower price per unit than before the tax is imposed, and the consumer pays a higher price than in the no-tax case. Therefore, part of the tax is paid by consumers in the form of a high pump price, and part is paid by the producer in the form of a lower after-tax price received.

The economic incidence of a tax is largely determined by the elasticities of supply and demand, that is, by the change in the quantity consumed or produced when the price of that good changes because of the imposition of the tax. When the price elasticity of supply is very small, the supply curve becomes more vertical and the supplier tends to bear a larger portion of the burden of the tax. When demand is very price inelastic, the consumer tends to bear a larger share of the burden of the tax (because there are few substitutes for the taxed good). This type of analysis can also be done for taxes on factors—that is, for taxes levied directly on labor and capital, such as a corporate profits tax or a payroll tax.

The analysis of tax incidence becomes more complicated when we consider the impact of a tax in one market on the supply and demand for goods in other markets. Arnold Harberger (1962), a pioneer of the study of general equilibrium tax incidence, demonstrated the theory that taxes levied in one market can be borne by productive factors in another market. Harberger’s model evaluated the impact of a corporate income tax as a tax on capital in one sector of the economy (a “partial factor tax”). By using a model in which the demand and supply for output adjusted to a new equilibrium after a tax was imposed, the impact of a corporate income tax on the price of capital, labor, and output could be analyzed. The results show that, depending on the elasticities of demand and supply and the ability of producers to substitute labor for capital in the production process, the burden of a corporate income tax could be fully or partially borne by labor or capital, or shifted forward in terms of higher output prices. Harberger’s model has been used since the 1960s to estimate the burden of taxes, and it is also a model for analyzing the excess burden or “welfare loss” of taxes.

Even more complicated, intertemporal models that consider the incidence of taxes over a lifetime have been developed using sophisticated models of the economy. John Shoven and John Whalley (1984) were among the first economists to use computer models to analyze the incidence of a system of taxes. These types of models are now regularly used as a means to incorporate many markets into the tax incidence analysis.

Joseph Pechman and Benjamin Okner (1974) produced one of the first comprehensive incidence analyses of the U.S. tax system, using incidence assumptions based on general equilibrium results. They compared the distribution of income before and after taxes (imposing various assumptions about the economic incidence of the tax) and showed that at that time, the tax system had little impact on the after-tax distribution of income. The Congressional Budget Office produces regular analyses of the distribution of the burden of U.S. federal taxes. Their 2006 analysis shows that when all federal taxes are considered, the tax system is somewhat progressive—that is, as incomes increase, so too does the percentage of income paid in tax.

Bibliography:

- Congressional Budget Office. 2006. Historical Effective Federal Tax Rates: 1979–2004. Washington, DC: Author. http://www.cbo.gov/ftpdoc.cfm?index=7000&type=1.

- Harberger, Arnold C. 1962. The Incidence of the Corporate Income Tax. Journal of Political Economy 70 (June): 215–240.

- Pechman, Joseph A., and Benjamin A. Okner. 1974. Who Bears the Tax Burden? Washington, DC: The Brookings Institution.

- Shoven, John B., and John Whalley. 1984. Applied General Equilibrium Models of Taxation and International Trade: An Introduction and Survey. Journal of Economic Literature 22 (September): 1007–1051.

See also:

Free research papers are not written to satisfy your specific instructions. You can use our professional writing services to buy a custom research paper on any topic and get your high quality paper at affordable price.

ORDER HIGH QUALITY CUSTOM PAPER

Always on-time

Plagiarism-Free

100% Confidentiality

{kind=link}