This sample High Tech Entrepreneurship Research Paper is published for educational and informational purposes only. If you need help writing your assignment, please use our research paper writing service and buy a paper on any topic at affordable price. Also check our tips on how to write a research paper, see the lists of research paper topics, and browse research paper examples.

The goals of this research paper are to introduce the reader to the current state of knowledge on high technology entrepreneurship and to identify questions that are not yet answered, are open for debate, and are in need of further empirical research. This research paper will discuss each of these items in turn, beginning with definitions and the importance of entrepreneurship, and turning next to the state of innovation in the U.S. innovation system and the sources of innovation. Next, moving through a typical sequence of start-up events, we identify significant issues that may create crises. We conclude with comparisons of the climate and institutional arrangements that support entrepreneurship in the United States and elsewhere.

Entrepreneurship And Its Importance

First, what is entrepreneurship, why is it important, and what is different about high technology entrepreneurship? While there are many definitions, we define entrepreneur-ship as a process of innovation that creates a new organization (new venture or start-up).1 An entrepreneurial venture is a relatively recently founded firm that is both young and small, but not by design and not for long. High technology entrepreneurs seek high growth and expect their ventures to develop into complex enterprises. Entrepreneurship thrives in countries whose national institutions and social norms support new venture creation and when collaboration is facilitated between industry, government, and educational institutions.

Entrepreneurship is important because it fosters economic growth. The rate of entrepreneurship surged throughout the world in the last quarter of the 20th century, thriving in countries as diverse as China, India, the Czech Republic, Turkey, Korea, Ireland, Peru, and the United States, according to the Global Entrepreneurship Monitor (GEM; 2006), a 42-country, 5-continent study of the dynamic entrepreneurial propensities of countries. GEM investigators reported that a country’s rate of entrepreneurial activity is positively correlated with national economic growth (measured as per capita GDP) over time, 1999-2006.

Entrepreneurs expand existing markets by identifying niches, thereby increasing competition and economic efficiency. They also create entirely new markets by developing innovative products as well as innovative applications and variants of existing product lines. New markets present profit opportunities to others, spurring further economic activity. Worldwide, the rate of early stage (nascent) entrepreneurship varies across countries from a low of 2.7% (Belgium) to a high of 40% (Peru), with the United States and Australia at 10% and 12%, respectively. However, this rate also depends on the demographic cultural and institutional characteristics of each country. Of the 24.7 million business firms in the United States in 2004, 99.7% employed between 10 and 200 people, accounting for 45% of the total private payroll, and just over half of 112.4 million workers in the nonfarm private sector. Small firms created 60% to 80% of the net new jobs annually for the last decade, and are more innovative than their larger counterparts, producing 13 to 14 times as many patents per employee. They also account for up to 80% of sales of new innovative products in the first years after launch. Patents filed by small businesses are twice as likely as those filed by large firms to be among the top 1% of patents in subsequent citations (U.S. Small Business Administration, 2006). These are the “high technology” small firms that offer wealth creation, jobs, and economic growth because they are so innovative.

High technology describes the “technology intensiveness” of a business or industry, which is often measured by money spent on research and development (R&D) as a percent of revenues to develop innovative products and technologies. The all-industry U.S. average research and development R&D/Sales ratio is 3.4%, varying from less than 1% to a high of 20%. High technology industries’ rates range from 8.3% for the U.S. semiconductor industry to 20% for the software industry. Other measures include the fraction of all employees involved in R&D or with advanced degrees or technical education. Biotechnology, nanotechnology, electronic device manufacturers, photonics, and medical instruments are considered technology-intensive industries.

What is “high technology” is relative to whatever else is available: It depends upon when you ask the question. In 1890, “high” or cutting-edge technologies included petroleum refining, street railways, machine tools, and telephones. In 1990, it was electronics and computers. By 2007, consumer devices like the iPhone and nanoengineered materials are high technology, as are genetically engineered medications that target specific diseases. What was “high technology” in one era quickly becomes the accepted norm in the next.

High technology entrepreneurship is the process of starting a new venture based on scientific advances or a technology not generally in use or not in use in the industry in question. Recognizing opportunity, gathering needed resources and people, structuring an organization and bringing the product to market are all aspects of new venture creation—and each can be challenging. High technology entrepreneurship differs from entrepreneurship in nonscience-based industries, because it creates a higher proportion of innovative products than nonscience-based entrepreneurship, accounting for the Small Business Ad-ministration’s patent citation counts and other measures of innovativeness previously mentioned. High technology entrepreneurship is also high in risk, because the market success of a new technology cannot be forecast (Rosenberg, 2000), and because new ventures face “liabilities of newness,” or a greater likelihood of failing than older, established firms (Stinchcombe, 1965; Schoonhoven, 2005).

High technology entrepreneurship is also potentially high in rewards, because new technology can transform whole industries and create new markets. Entrepreneur-ship is the most likely entry to market for new, “disruptive” technologies—those that change the way business is done, rendering older methods obsolete (Tushman & Anderson, 1986). Established firms tend to improve existing technologies and products, rather than introducing wholly new ones.2 Innovation does take place in large corporations. Consider, for example, IBM’s development of the System 360 (Chandler, 2001), Texas Instruments’ introduction of commercial silicon transistors (Jelinek, 1979), or Monsanto’s shift into biotechnology (Day & Jelinek, 2007). Because significant innovations are rare in established firms, we focus on entrepreneurship, new ventures, and start-ups.

Would-be entrepreneurs must find new technologies, generate viable commercial applications, mitigate risks, create profitable paths to market, accumulate the necessary resources to proceed, and organize all this into a new, independent entity. New businesses fail at a higher rate than older, more established firms, especially businesses based on new science and technology. Yet it is difficult to predict which new ideas, innovations, and technologies will succeed to yield the new jobs, wealth, new industries, and new technology applications that make high technology entrepreneurship so attractive. Dell Computer Corporation, a well-known exemplar, began as a part-time business in a college dormitory room, but became the world’s largest personal computer firm with worldwide sales and market capitalization of more than $50 billion by 2007, about 15 years after its founding. Dell’s highly information-intensive business model uses computers and the Internet to serve both consumer and corporate customers and set new standards for service, delivery, and convenience.

But how do innovations and new technologies come into commercial use? Where do the ideas come from in the first place, and how do they come to be accepted? We turn first to a brief survey of selected frameworks about entrepreneurship and then to innovation and technical entrepreneur-ship in the United States.

Theories Of Entrepreneurship

Joseph Schumpeter (1936, 1940/1950), an early-20th-century economist, argued that innovation by entrepreneurs led to “gales of creative destruction” as innovations caused old products, ideas, technologies, skills, and equipment to become obsolete. More contemporary researchers concur that new technology drives economic growth by displacing older expenditures of capital, labor, and time as well as providing goods and services formerly unavailable, or available only to the very wealthy, as well as longer life, and better health (North, 1981, 1990; Rosenberg, Landau & Mowery, 1992).

Yet despite centuries of scholarly attention, no general theory about entrepreneurship has emerged, nor have substantive disciplinary theories of entrepreneurship, so we cannot systematically compare alternative theories (Schoonhoven & Romanelli, 2001). Instead, we consider five frameworks that have evolved to account for the phenomenon:3 two are “macro” frameworks that examine the firm in its external environment, industry, and institutional context; two others are “micro” frameworks addressing entrepreneurs and entrepreneurial teams. The social network approach to entrepreneurship, which we will discuss last, lies in between.

Liability of Newness

At the macro level, both theory and research show new organizations failing more often than older firms, the so-called “liability of newness.” All organizations are dependent upon and constrained by their social system, but new organizations must create new roles, a process that is time consuming, may involve trial-and-error learning, has the potential for interpersonal conflict, and is imbued with inefficiencies in execution of the new roles and the venture’s work (Stinchcombe, 1965).

New ventures rely primarily on social relations among strangers, and interpersonal trust is initially low among strangers, so relationships are precarious. Loyalty and thus the commitment to the venture’s goals are also uncertain— complicating efforts to efficiently execute a business plan. Lastly, new ventures typically lack external legitimacy, so establishing relationships with potential customers and suppliers is difficult: new organizations must start from scratch. Where existing rival organizations have strong ties to customers, it is more difficult for the new organization to displace rivals. Despite the difficulty of first gaining customers, the greater those customers’ reliance on the new product or service, the greater their stake in the venture’s survival. It is not unusual for customers to invest in new ventures that supply critical products or services.

Less obvious “social conditions” affecting new firms’ survival include a nation’s institutional framework. For some 40 years after World War II, private property was outlawed in China under its communist government. Entrepreneurs were not allowed to join the Communist Party (the sole political party) until the late 1990s, and the political institutions of China did not support the founding of new ventures. In Japan, which has a history of economic domination by a small number of very large industry groups (the kieretsu), entrepreneurship is still not common (although it is becoming more so among the young). “Lifetime employment” by a large company was the prevailing social ideal, and it remains socially shameful to be laid off, fired, or out of work in Japan, especially for a man. Japan’s institutions have not favored high technology entrepreneurship; most Japanese technology firms began as subsidiaries of much larger firms, rather than as independent start-ups. Japan and China have different institutional arrangements than the United States, and thus different social conditions.

New firms in science-based industries face an additional liability in their search for innovation (Schoonhoven, 2005). The time required to create new product knowledge is uncertain, making it difficult to predict when the first working prototype will be complete, or when income from first sales will be realized: The new firm must spend cash without revenues to support itself for months longer than expected, and those attempting highly innovative products take longer to reach first revenues (Schoonhoven, Eisenhardt et al., 1990), raising the likelihood of failure.

Why are newness liabilities important for a potential entrepreneur? The simple fact that new firms fail at a higher rate than established firms describes the relatively high risk as well the substantial challenge of high technology entrepreneurship. For a discussion of practical actions entrepreneurs might take to mitigate these liabilities of newness, see Schoonhoven, 2005. Good textbooks on entrepreneurship also review multiple sources of risk for a new venture, along with risk mitigation strategies (e.g., Timmons & Spinelli, 2007).

Death Rates: Industry Size, Legitimation, and Competition

One prominent framework argues that as the number of new firms in an industry (called a population) increases, the death rate of new firms decreases. However, after a certain point, death rates increase again. Referred to as “density-dependent death rates” (Hannan & Carroll, 1992), this same relationship has been found in a wide range of industries such as credit unions, telecommunications, semiconductors, newspapers, and hospitals (e.g., Barnett & Carroll, 1987; Ruef, 1997). The practical implication is that death rates of new firms differ as industry size increases over time; first movers face a particular challenge.

Researchers argue that population density—the number of firms in an industry—determines both the level of legitimation of the industry and the degree of competition within it (Hannan & Carroll, 1992). As density increases, legitimation also increases—until, after a certain point, further density creates greater competition for resources, driving up mortality rates. There are several practical implications of these ideas. An entirely new type of organization—the first of its kind—will struggle to establish its legitimacy with other suppliers and customers and thus face greater likelihood of death. As other new firms enter, the industry’s increasing density increases legitimation for all, improving the likelihood of survival for any given firm. As more firms compete, death rates increase again because there are too many firms competing for similar resources, creating an industry “shake out” when the less fit firms fail.

Entrepreneurial Characteristics

Microlevel research investigates entrepreneurs (who range from “entrepreneurs by necessity,” such as indigents who start street stalls in underdeveloped countries, to the technical specialists who start high technology businesses). Conventional wisdom holds that entrepreneurs are more comfortable with risk, more achievement oriented, and more self-directed. Ethnic minorities, women, and immigrants are often entrepreneurs—perhaps because of barriers to entry or advancement in mainstream businesses, or a desire for more personal control over outcomes. However, classic personality trait research has not been able to predict who will become an entrepreneur or who will succeed. Yet important psychological and cognitive variables such as differences in opportunity recognition, expectancies for performance, and attributions do distinguish entrepreneurs.5

Key characteristics of entrepreneurs center on their ability to recognize opportunities: This ability is a function of their personal networks; their ability to think “outside the box” of conventional thought; their personal experience; or their ability to see that their problem is also the problem of many others. Entrepreneurs are often highly networked: Their wide social contacts link to key resources. A review of entrepreneurship dynamics highlights these distinctive capabilities—but we focus on high technology entrepreneur-ship dynamics per se, rather than on entrepreneurs’ personal characteristics.

Teams of Entrepreneurs

Because small businesses tend to be relatively simple undertakings, they are often started by a single individual. By contrast, new high technology firms tend to be founded by teams of entrepreneurs (Boeker, 1989; Schoonhoven, Eisenhardt et al., 1990). One reason is that entrepreneurship is a social network process (Aldrich, 1999): Most of the resources required to start a new venture must be obtained through others, including introductions to potential investors and help recruiting key talent. Ventures founded by a team of entrepreneurs will enjoy larger and more diverse networks—individual members’ networks multiplied by the number of founders on the team (minus any redundant elements of their networks).

Then, too, the tasks required to found a new high technology venture are complex, and can easily overwhelm the knowledge, experience, and available time of any single individual. Contemporary science-based technologies are typically multidisciplinary, requiring the input and collaboration of multiple specialists to bring a new product or service to fruition. Among new science-based ventures, firms founded by fully staffed teams (that is, those having top management members who cover all critical business functions) bring first products to market faster than less adequately staffed teams (Schoonhoven, Eisenhardt et al., 1990). Ventures developing a new technology product must rapidly build key capabilities within the first year, attracting quality personnel in essential functional areas and building functional integration across the new organization, which speeds first products to market. Ventures lacking key staff will lag in building such integration.

New ventures benefit from a “strong” founding top management team of three or more members with a range of industry and functional experience in addition to more recently trained technical experts. Ventures with strong founding top management teams have the highest revenue growth rate in their first four years (Eisenhardt & Schoonhoven, 1990), a higher probability of reaching $20 million in revenues, and a higher probability of going public (Schoonhoven,Woolley, & Lyman, 2007). A strong team’s variety can also be reflected in its diverse social network.

Entrepreneurship as a Social Network Process

A growing body of research sees entrepreneurship as a social network process in which entrepreneurs draw on their personal networks for information, advice, and specialist expertise—capabilities not yet developed in the start-up. In short, networks can provide a firm with access to a wider range of resources, information, markets, and more (Gulati, Nohria et al., 2000)—the resources entrepreneurial start-ups need to recognize opportunities (Cooper, 2001) or compete effectively (McEvily & Zaheer, 1999).

Networking with established firms can provide an array of benefits including social capital (Tsai, 2000), trust (Kale, Singh et al., 2000), and access to the broader network’s resources through informal as well as formal relationships (Kogut, 2000) for both U.S. and non-U.S. entrepreneurial firms (Lee, Lee, et al., 2001). Other benefits include credibility or legitimacy—like vouching for the quality of technology or new products (Cooper, 2001). Such links are most valuable when they are complementary to the skills, capabilities, and resources of the entrepreneurial firm (Chung, Singh, et al. 2000); when they stimulate new learning or capability (Hitt, Dacin, et al., 2000); or when they provide resources the entrepreneurial firm lacks altogether (Starr & MacMillan, 1990; Dubini & Aldrich, 1991). Further benefits from networking, alliances, and similar ties accrue for independent as well as “corporate entrepreneurship” efforts.6 In short, network ties are critical to successful entrepreneur-ship. We turn next to the U.S. innovation system.

Brief Tour Of The U.S. Innovation System

Because the United States has been the most prolifically entrepreneurial society, there is great worldwide interest in the U.S. innovation system, how it works in comparison

to others, and whether its approaches can be adopted elsewhere. We turn first to the U.S. innovation system and its sources of innovation. Next, we identify critical start-up issues. We conclude with comparisons of the institutional arrangements that affect entrepreneurship in the United States and in selected other countries. Our tour of innovation and technical entrepreneurship in the United States begins with the relationships between U.S. universities and industries, patent and bankruptcy laws, and entrepreneurship.

A typical innovation path envisions a scientific discovery that is refined in the laboratory by countless small insights, and then moved into “development”—to apply the ideas to a new or existing commercial product or service need. An open marketplace for ideas means that others refine the original ideas, so the economy becomes increasingly efficient as entrepreneurs apply new knowledge. Such macro perspectives embrace economic theory, industry, geographic analysis, and business history studies of entrepreneurship, as well as the “institutional” factors that comprise the national framework of laws and systems within which entrepreneurship occurs.

U.S. patent law grants the innovator a limited monopoly to exploit a discovery, in return for disclosing its details. This law is written into the U.S. Constitution. Americans were renowned as innovators from the earliest days of the country—and as adopters of others’ technology, much as the Chinese, Koreans, and Indians are seen today—well into the 20th century. Global trading relations in the World Trade Organization (WTO) hinge on extensive diplomatic negotiations about intellectual property (IP) rights—that is, patent and copyright ownership, licensure, and protections. Developed-country innovators want their IP protected so that others must pay to use inventions; developing country users want access to products or ideas they see as essential. Current disputes between developed economies like the European Union and the United States, and the less devel-oped economies like China and India include pharmaceuticals (especially drugs for HIV-AIDS), bioengineered crops (such as RoundUp Ready™ cotton or soybeans), and video, music, software, and other digital IP.

U.S. universities receive most federal research funds and are the source of most basic scientific discoveries as well as trained students to work in industry. Hundreds of public universities (such as the University of California and similar schools in every state) are supported by state legislators interested in economic development and by industrial firms eager to sponsor research to solve their problems. One result: U.S. colleges and universities have historically been highly responsive to industry needs—generating whole new disciplines like petroleum engineering and aeronautical engineering, computer systems and materials science (and graduates trained in them) well before European or Asian universities.

About 80% of U.S. federal funding for scientific research since World War II is given to universities and is aimed at “fundamental” research with no commercial application necessarily in sight. Industries can sponsor (or perform) further research into commercial applications to generate proprietary IP. Since researchers’ students often go into industry, much new knowledge is transferred directly through them, or otherwise “leaks” into commercial firms (some sources estimate that as much as 95% of new knowledge is transferred by these means, rather than by the much more widely mentioned—and hotly contested—technology licensing efforts by universities).

Close relationships between the U.S. military and its suppliers, particularly firms in the aeronautical, communications, and computer industries, have also helped fuel U.S. high technology entrepreneurship. Billions of dollars of investment in military and technical space research has given rise to commercial semiconductor electronics (leading to an explosion of computer and telecommunications devices), the Internet (initially a Department of Defense communications link), and global positioning technology (at first available to civilians only in a degraded signal, now routinely included in automobiles and cell phones, and in handheld devices for hikers). Government-supported research is also conducted within federal laboratories, National Aeronautics and Space Administration (NASA), and National Institute of Standards and Technology (NIST), among others.

These close relationships have favored technology and science research and its eventual commercial application to a greater degree in the United States than in many other countries.8 Historically, the United States has invested substantial amounts on research and education relative to other countries, while other countries lacked the requisite infrastructure for research with links between laboratories and commercial firms. The era from 1950 to 2000 saw tremendous scientific, technical, and economic growth in the United States and in other countries. This growth boosted investments to foster similar technology transfer: When the United States launched its National Nanotechnology Initiative in 1999 with some $2 billion of research investment, other countries also invested heavily, so that U.S. nanotechnology expenditures have remained at only about 28% of the global total, despite the increase. By contrast, especially after World War II, the U.S. investment dwarfed that of all Europe and Asia for decades.

The Bayh-Dole Act and university Entrepreneurship

Many sources cite the Bayh-Dole Act9 of 1980 as the spur for U.S. university interest in commercially valuable research, technology innovation, and licensing. Bayh-Dole permitted universities to take title to federally funded discoveries made on their campuses. Since most university research is federally funded in the United States, in practical terms the universities took title for all discoveries made on their premises by faculty, staff, or graduate students, clarifying ownership and the right to license. Despite economic theory arguments that incentives are critical to encourage risky technology development investments (Teece, 1986), technology licensure has produced few big winners for universities—and all of these were broadly licensed, sometimes to hundreds of firms (thus undercutting the argument that exclusive ownership was required to commercialize technology). The (very) few enormously valuable discoveries that seemed to corroborate the assumed value of licenses are almost all in biotechnology.

No sharp change in university research behavior, quality, or focus is discernible before or after Bayh-Dole (Mowery, Nelson et al., 2004). Direct return on investment from licensing per se is not great. A small number of “home runs” have earned universities huge returns; but most university patents are never bid upon (80% of those that are have only one bidder). Just as most university knowledge passes into use through students’ learning and subsequent employment, or through publications rather than licenses, most benefit to universities comes not from license revenues but from sponsored research, outright donations, political support before state legislatures, and other ongoing relationships with industry partners.

For the potential entrepreneur, universities and federal labs offer rich prospects for new technologies, much of which has never been bid upon. This basic research is sometimes wholly public, opening the door for further development of potentially proprietary knowledge. Basic research can be accessed through classes, published research papers, and public lectures; through consultation arrangements with faculty; student internships and sponsored research; and by means of consortium membership, where industry members or firms with common noncompeting interests collectively fund research (leveraging members’ individual contributions), in addition to the more widely mentioned licensing agreements.

A plethora of online sources is also available: The National Science Foundation’s research grants are described online, and U.S. research university Web sites describe research and link to technology transfer offices to facilitate licensing discoveries. Numerous consortia—in the form of industry-university cooperative research centers, such as Auburn University’s Center for Advanced Vehicle Electronics or the Center for Research on Information Technology and Organizations (CRITO) at the University of California at Irvine10—undertake collaborative research on topics of interest and publish their results. Member companies may enjoy first right of refusal for commercial use of discoveries they have funded. Universities are also potential sources of knowledgeable employees, consultants, and researchers, all of whom conduct further research. New companies with close university relations have higher survival rates.

The Path From Discovery Science To Commercial Deployment

Once a promising new science or technology is discovered, the next challenge is to recognize a potential application and develop it sufficiently to create marketable products. University inventors may be unaware of commercial potential or may not want to commercialize their discoveries. This makes opportunity recognition a key crisis point—both a failure point for many technologies and an opportunity point for observant entrepreneurs.

A nascent technology is typically far from commercial viability: Further development is needed to explore its possibilities, reduce uncertainty, assure reliability or safety, or to lower cost before the new idea is ready for the marketplace. Alternatively, some ideas are accepted so enthusiastically that one wonders why they weren’t thought of before (such as the Sony Walkman, iTunes, or Post-its).

Another constraint is that some innovations require enabling technologies. For example, an iPod or laptop computer that can stream video and music depends on high-speed digital data transfer and low-cost memory to capture downloads. Commercial air travel required dependable internal combustion engines, lightweight and strong aircraft components, and innovations to insure the safety of naive civilian passengers. Google became ubiquitous only when powerful servers and proliferating Web site content made the Internet a cornucopia of information through efficient Web browsing. New technologies may erode once rock-solid businesses—as video rental stores give way to Netflix’s DVDs by mail and to online downloads. Integrating technologies—for example, Apple’s iPhone, which combines a revolutionary mobile phone, a wide-screen iPod with touch controls, and Internet access—can reduce demand for products they replace: Schumpeter’s creative destruction in action. The need for enabling and complementary technologies means that genuinely new-to-the-world high technology entrepreneurship is risky. It can also be highly lucrative, since “disruptive technology” that obsoletes existing methods can vault the entrepreneur into market leadership for decades to come (Chandler, 1990). These same relationships among technologies help explain why networks of relationships among firms are essential and why certain regions of the world dominate particular industries over time (Porter, 1990; Krugman, 1995; Romanelli & Schoonhoven, 2001). Silicon Valley is the innovative model that many localities seek to reproduce in hopes of creating jobs and wealth from science, but replication is not easy.

The Silicon Valley Archetype

California’s Silicon Valley, the area that extends south from San Francisco to San Jose, is the envy of countries around the world. Emulators like Scotland’s “Silicon Glen” and Manhattan’s “Silicon Alley,” a concentration of Internet and new media companies, and “Silicon Orchard” in Northern Ireland (among many others) testify to widespread admiration. What’s so special about Silicon Valley that so many countries should seek to duplicate some version of it? In short, successful high technology entrepreneurship.

Silicon Valley is home to multiple intellectual resources: most notably world-class researchers and graduates from Stanford and the University of California at Berkeley, many leading-edge technologies, and financial assets available through venture capitalists and angel investors (many of whom are successful entrepreneurs themselves who have “cashed out” of their businesses), legal experts and deal makers—plus experienced venture managers used to dealing with start-ups (Kenny, 2000; Saxenian, 2000; Suchman, Steward et al., 2001).

These knowledge resources have fostered new ventures for decades in a succession of technologies. Resources in close proximity lower the risk of starting a new venture. Clusters of high technology-oriented support firms— specialists in advanced computing, or manufacturing processes, accounting for new ventures or drawing incorporation papers, advertising, or staffing—make Silicon Valley a highly supportive area in which to start a firm. Because start-ups and entrepreneurship are “in the air,” Silicon Valley is exciting: There is always something new happening (Lee, Miller et al., 2000).

Successful high technology entrepreneurship has also driven up prices for real estate and salaries, created problems dealing with congestion, and increased pollution, creating an outflow of firms, or at least branches, with their technical talent, and thus the spread of Silicon Valley emulators as entrepreneurs seek to recreate the “habitat for entrepreneur-ship” (Lee, Miller et al., 2000). Beyond U.S. locations—i.e., Oregon (“Silicon Forest”) and Arizona (“Silicon Desert”)— foreign governments, most notably China, Taiwan, and India, have created technology development zones or science parks to attract entrepreneurs to start new firms (Li et al., 2007). They also seek Silicon Valley “graduates”—many of whom first arrived in the United States as foreign students to attend California universities—for job opportunities back home (Saxenian, 1999, 2000).

Yet it is difficult to duplicate the successes of Silicon Valley elsewhere; the U.S. innovation system’s close relationships between universities and their researchers and entrepreneurs and supporting businesses are unusual. U.S. venture capitalists’ access to capital, ability to recognize opportunity and nurture start-ups, and willingness to invest in what may be no more than a dream that is far from commercial realization are also hard to duplicate. U.S. laws that facilitate investments by venture capitalists and others, including the billion-dollar pension funds and institutional investors that provide capital for venture capital firms, are still unique in the world today.

The U.S. system of patents and licenses for IP is another element of the puzzle: For all its difficulties (Jaffe & Lerner, 2004), the system has encouraged numerous high tech start-ups. Economists have long argued that strong patent protection encourages innovation by assuring economic incentives for inventors. Patterns of technology citations in patents, locale, and associations among patent holders offer a revealing look at the networks of familiarity and communities of interest that generate new technologies. Online resources include the U.S. Securities and Exchange Commission’s database (see especially the S-1 forms filed by nascent firms seeking IPOs), while extensive patent data are also available to individual users (Jaffe & Trajtenberg, 2002).

Personal bankruptcy laws encourage entrepreneurial risk taking by protecting U.S. entrepreneurs from losing their homes and personal effects if their business fails. As a consequence, the U.S. innovation system permits failed entrepreneurs another chance. So-called “serial entrepreneurs” are an especially interesting research topic, both because successful entrepreneurs can self-fund for subsequent ventures, and because their prior success predisposes others to back their proposals.

We have been discussing “institution-level” factors, insofar as they concern federal laws and the U.S. national innovation system, and “regional factors,” insofar as they describe unique characteristics of particular regions (such as Silicon Valley). There is no single, simple recipe for success. The perfect mix of factors to foster new ventures varies—by region, the underlying science or technology involved, the nature of the extant industry and the potential new industry, and the availability of start-up resources of all kinds. Even Boston’s Route 128, which enjoyed leading universities and even the very first high technology venture capitalists, has not been as successful at fostering entrepreneurship as Silicon Valley, with differences attributed to Silicon Valley’s regional network-based industrial system, its greater flexibility and technological dynamism, and collective learning (Saxenian, 1994). In contrast, Route 128 firms are described as more atomized and secretive, and their employees are much less mobile across companies in the region, which do not welcome “traitors” from other firms. The challenge is even greater in other countries, where university researchers are government employees who must resign their pensions to start a firm; or where going bankrupt is considered a social shame for the entrepreneur and his family, perhaps for generations; or where national governments are so weak that corruption makes ownership risky (Pearce, 2001). Still, Americans (whether native born or immigrants) have no monopoly on entrepreneurship. A closer look at entrepreneurship in China will illustrate some crucial differences in that country’s national innovation system.

Entrepreneurship In Contemporary China

After decades without private ownership or foreign investment, the Chinese government slowly opened its economy in the 1980s, then established national technology development zones (TDZs) to encourage local entrepreneurship in high technology industries, including electronic information, integrated optical and advanced manufacturing, biotech and pharmaceuticals, new materials, new energy, aeronautical engineering, ocean technology, high technology agriculture, environmental protection, and nuclear applications.

Some 5,000 new ventures were reportedly founded in the Beijing TDZ between 1988 and 1998 (Chen, 1998), while the China Statistics Yearbook (1999), reported that 16,097 new technology-intensive firms existed in China in 1998. Reynolds and colleagues (2001) assert that entrepreneurial activity in a country is positively associated with national economic growth. But Of the 5,000 new ventures founded in the Beijing TDZ between 1988 and 1998, only 9% survived 5 years (Chen, 1998), and only a miniscule 3% survived to their 8th year of life. Survival rates of 60% and 62% for new firms in the United States and Germany are far more robust than for Chinese firms: A 20 to 21 times greater proportion of new U.S. semiconductor firms survived to year 8 than did Beijing firms (Schoonhoven & Woolley, 2007).11

The high death rates of the Chinese companies demonstrate that economic incentives alone are not adequate for new firms to prosper. We are again reminded of the complex network of interrelated technology and service firms located in close proximity to one another in the Silicon Valley region, along with an inclination in the region for firms to collaborate and form strategic alliances.

High Technology Entrepreneurial Dynamics

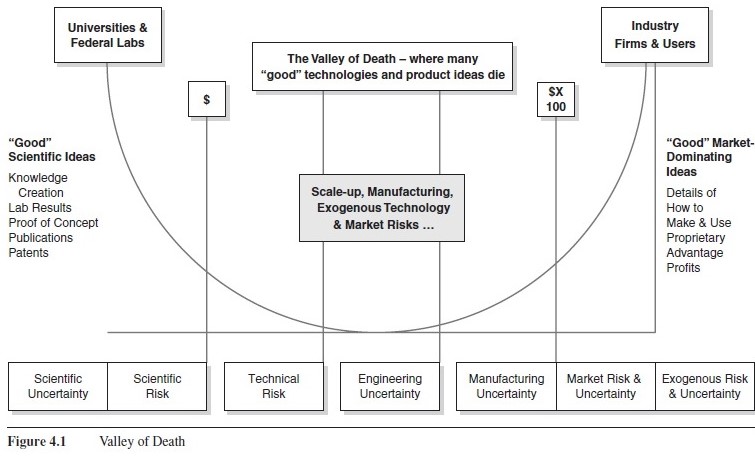

Researchers into new product development often speak of the “fuzzy front end” of innovation—the early days of an idea or a scientific discovery or of a new product development effort when much is uncertain. Who will want the new technology? What aspect of it is important? For what price? How will it be manufactured and utilized? Even valuable science and technology ideas may fall into the Valley of Death-an area of “no funding available”—because the ideas are insufficiently developed to attract money for commercial development.

Where university research is funded by scientific grants (typically from federal programs) and dedicated exclusively to an agreed-upon project, development expenses in a new firm compete with many other claims for cash. Moreover, when the Valley of Death begins after an initial discovery, research funds disappear before commercial funds can be attracted, because a vast developmental distance may loom before the product can be bought to market. Figure 4.1 highlights some of the difficulties.

In Figure 4.1, the left side is identified as the point of discovery. The landmark discovery of recombinant DNA at the University of California, San Francisco, is a good example. The first genetic engineering experiments in 1973 and the first biotechnology firm, Genentech, was founded in 1976. Yet enabling discoveries were required to launch the biotech industry. The polymerase chain reaction was not well understood until 1980 (Rabinow, 1996) and was not commercially practical without the DNA micro arrays pioneered by Affymetrix that permitted rapid gene prototyping under computer control (Robbins-Roth, 2000). The scale of needed funds was enormous. First-generation biotech companies founded between 1980-1986 raised $578.3 million at initial public offerings (IPOs; Robbins-Roth, 2000) to carry on this development. In the next 2 years, $534 million was raised, and the dollars increased thereafter. These huge sums are mere entry stakes, not guarantees of success.

Figure 4.1 Valley of Death

Figure 4.1 Valley of Death

As Figure 4.1 suggests, commercialization faces a series of hazards, any one of which can be a showstopper. Development research must assure that an innovation can be produced reliably and with acceptable manufacturing costs and yields. If the buyer is another firm, the innovation must fit into customers’ downstream production processes (Jelinek, 1996, 1997) and needs at least a 20% improvement in performance or cost (Foster, 1986) to overcome the buyer’s reluctance to change.

In the case of DNA-based pharmaceuticals, large companies lacked the human resources, equipment, and experience to carry on their own DNA research (graduates from before around 1976 would have no familiarity with the DNA science), so start-ups were the route for this technology to reach the marketplace. Yet, start-ups lack the massive resources, expertise, and capabilities needed for clinical trials to acquire U.S. Federal Drug Administration (FDA) approval, which entails three stages of clinical tri-als to prove that the drug works, that it works better than other therapies, and that it does so with acceptable risks and consequences for patients. On approval, the new product faces market competition from other products, old and new, and agreement (or not) by third-party payers, the insurance companies, to pay for patients’ use. Given such complexity of development, it’s scarcely surprising that high technology entrepreneurship is risky.

While the path from discovery to market is often described as a funnel that narrows down paths to the final goal, it is better described by the analogy of ants hauling morsels across a beach, over monumental sand dunes, grain by grain: If one particular direction doesn’t work, try another to find some path forward (Sarasvathy, 2001). The case of the commercialization of lasers illustrates this point: initially a laboratory toy, then considered as a possible weapon, lasers today are used to cut materials, inscribe information on surfaces, read barcodes by cash registers, open doors, and perform surgery on human eyes (e.g., LASIK eye correction). None of these applications could have been readily foreseen in the early days of lasers (Rosenberg, 2000). Accounts by entrepreneurs offer validation on a much more immediate level (e.g., Lusk & Harrison 2002), corroborating the changes in direction and intent that often emerge in the messy, uncertain processes of entrepreneurship.

Building the Firm

Even with stable technology and application(s) in hand, entrepreneurs must acquire personnel, facilities for development, and critical expertise. The nascent firm must stabilize operations and increase revenues and profit from its now-launched technology. Should the new product fail despite wonderful technology, investors may withdraw to doom the company before a second chance: Their agenda is financial gain, not technology. Early in new markets, when no industry standard exists, multiple product configurations compete. In the early 20th century, steam and electric automobiles far outnumbered gasoline-powered cars—which nevertheless eventually dominated, driven in large measure by Henry Ford’s production line and dramatically lowered manufacturing costs that dropped the price of a personal gasoline-powered automobile. While internal combustion engines dominate today, that basic configuration is under pressure from hybrids and electric cars—and new ventures and entrepreneurship threaten “creative destruction” even in this old, mature market, and even of long-dominant firms like General Motors and Ford Motor Company.

Conclusions

Our brief survey of high technology entrepreneurship suggests that the field still lacks a general theory of entrepreneurship or even substantive partial disciplinary theories. We noted that economists, business historians, and sociologists have been fascinated by the macro phenomenon of entrepreneurship, pointing to national innovation systems and their characteristics that seem to foster (or inhibit) entrepreneurship. At a micro level, while studies of individual entrepreneurs’ traits have not proven helpful in predicting who will become an entrepreneur or who will succeed, important cognitive differences do seem important, especially those that relate directly to the tasks of entrepreneurial start-ups—like opportunity recognition. Our brief tour of the Valley of Death linked research findings about the hazards facing any new product with insights on crises facing entrepreneurs and their start-ups. Social networking stands between micro and macro levels and helps to illustrate just how entrepreneurs and their teams bridge the gap between idea and marketplace reality. Entrepreneurship is important, risky, exciting, and ripe for further inquiry and achievement.

References:

- Acs, Z. J., & Audretsch, D. (Eds.). (2005). Handbook of entrepreneurship research: An interdisciplinary survey and introduc-tion. New York: Springer.

- Baum, J. R., Frese, M., et al. (Eds.). (2007). The psychology of entrepreneurship. Mahwah, NJ: Lawrence Erlbaum Associates.

- Gartner, W. B., Shaver, K. G., et al. (Eds.). (2QQA). Handbook of entrepreneurial dynamics: The process of business creation. Thousand Oaks, CA: Sage.

- Hitt, M. A., Ireland, R. D., et al. (2QQl). Guest editors’ introduction to the special issue; Strategic entrepreneurship: Entrepreneurial strategies for wealth creation. Strategic Management Journal, 22(6/7, Special issue), A79-A9l.

- Lusk, J., & Harrison, K. (2QQ2). The mouse driver chronicles: The true-life adventures of two first-time entrepreneurs. Cam-bridge, MA: Perseus.

- Mowery, D. (l998). The changing structure of the U.S. national innovation system: Implications for international conflict and cooperation in R&D policy. Research Policy, 27(б), 639-654.

- Mowery, D. C., & Rosenberg, N. (l998). Paths of innovation: Technological change in 20th-century America. Cambridge, UK: Cambridge University Press.

- Rosenberg, N., Landau, R., Eds. (1992). Technology and the wealth of nations. Stanford, CA: Stanford

- University Press. Rogers, E. M. (2003). Diffusion of innovations. (5th ed.). New York: The Free Press.

- Schoonhoven, C. B. & Romanelli, E. (Eds.). (2QQl). The entrepreneurship dynamic: Origins of entrepreneurship and the evolution of industries. Stanford, CA: Stanford University Press.

- The Global Entrepreneurship Monitor Web site, http://www.gem-consortium.org/ for much additional information and data on entrepreneurship in numerous participating companies, as well as information about the Global Entrepreneurship Monitor program.

- The U.S. Securities and Exchange Commission Web site, http:// www.sec.gov for much information on business firms, including form S-l which entrepreneurs must file before an Initial Public Offering.

See also:

Free research papers are not written to satisfy your specific instructions. You can use our professional writing services to order a custom research paper on any topic and get your high quality paper at affordable price

ORDER HIGH QUALITY CUSTOM PAPER

Always on-time

Plagiarism-Free

100% Confidentiality

{kind=link}