This sample Supply Research Paper is published for educational and informational purposes only. If you need help writing your assignment, please use our research paper writing service and buy a paper on any topic at affordable price. Also check our tips on how to write a research paper, see the lists of research paper topics, and browse research paper examples.

In economic theory, supply is the relationship between the price of a product and the number of units of product that producers are willing to offer for sale per unit time (called quantity supplied) when all other relevant factors, excluding the price of the product, remain fixed. The concept of supply ignores the effect of consumers on the market by assuming that consumers purchase as many units as producers offer for sale. The assumption that other factors remain fixed is known as the ceteris paribus assumption. For example, suppose that when the price of a product is $10 per unit, producers are willing to offer one million units of product for sale each month (the quantity supplied). Holding all other things constant, if the price of the product were to rise to $12, producers would make more profit on each unit and so producers would be enticed to offer more units for sale—the quantity of units supplied would rise. Similarly, holding all other things constant, if the price of the product were to fall to $8, producers would make less profit on each unit and so producers would be enticed to offer fewer units for sale—the quantity supplied would fall. Supply is this positive relationship between price and quantity supplied. Plotting various prices against the corresponding quantities supplied yields a graph called the supply curve. The supply curve is a pictorial representation of supply.

A shift in supply (also called a change in supply, or a supply shock) occurs when the number of units producers are willing to offer for sale changes for a reason unrelated to the price of the product. A shift in supply represents a new relationship between price and quantity. For example, suppose producers are willing to offer one millionunits of product for sale each month when the price per unit is $10. An increase in the costs of labor and materials reduces the producers’ profit margins and so reduces the producers’ incentives to produce. As a result, even if the price of the product were to remain fixed at $10, producers would no longer be willing to offer one million units of product for sale each month. Alternatively, suppose that a change in technology enables producers to produce at a fraction of the cost at which they used to produce. The new technology increases the producers’ profit margins and so increases the producers’ incentives to produce. As a result, even if the price of the product were to remain fixed at $10, producers would be willing to offer more than one million units for sale each month.

Most supply shocks (or violations of the ceteris paribus assumptions for supply) can be categorized as:

- changes in the prices of factors;

- changes in the technology the firm employs; and

- changes in the number of firms in the industry.

Factors are things the firm uses in producing its product. Examples of factors are labor, materials, energy, buildings, machinery, and land, the last three of which are a special type of factor called capital. Capital factors are factors that are used in the production of the product but that are not used up in the production (except in the sense of depreciating). Noncapital factors (labor, materials, energy) are used up in the production. For example, a firm uses steel and robots to produce cars. The steel that is used to produce one car cannot be used to produce a second car because the steel was used up in the production of the first car. The robot, however, can be used to produce one car and then used to produce a second car. The robot is not used up when the first car is produced. Therefore, the robot is a capital factor and the steel is a noncapital factor.

When the price of a factor declines, it becomes more profitable for producers to produce, so quantity supplied increases even if the price of the product remains constant. This is an increase in supply. Similarly, when the price of a factor increases, it becomes less profitable for producers to produce, so quantity supplied decreases even if the price of the product remains constant. This is a decrease in supply.

Technology is an intangible that represents the sophistication of the production process. For example, one hundred workers can produce one car every six months when each worker works on his own car. But, when the workers are arranged in an assembly line with each worker performing a specialized task, the one hundred workers can produce one car every day. The rearrangement of the workers into an assembly line is an improvement in technology. Prior to the invention of the Bessemer process, it was so difficult to refine aluminum that aluminum was more expensive than gold. In the 1800s Henry Bessemer discovered that injecting oxygen into the aluminum while it was melted allowed far more aluminum to be refined for the same cost. This discovery was an improvement in technology.

When technology improves, it becomes more profitable for producers to produce and so quantity supplied increases even if the price of the product remains constant. This is an increase in supply. If technology were to devolve, it would become less profitable for producers to produce, so quantity supplied would decrease even if the price of the product remained constant. This would be a decrease in supply.

The number of firms in the industry typically changes as the industry’s profitability changes. If the industry becomes more profitable than other industries of comparable risk, new firms will enter the industry, thereby increasing supply. If the industry becomes less profitable than other industries of comparable risk, existing firms will leave the industry, thereby decreasing supply.

When the number of firms in an industry declines, the quantity supplied decreases even if the price of the product remains constant. This is a decrease in supply. When the number of firms in an industry increases, the quantity supplied increases even if the price of the product remains constant. This is an increase in supply.

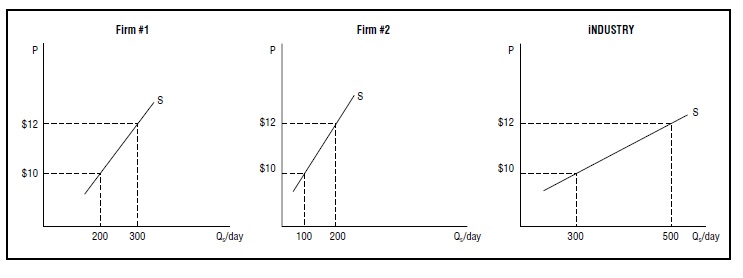

Supply (sometimes called industry supply) typically refers to the aggregate production of all firms in an industry. One can refer to the supply of a single firm (the individual supply, or firm’s supply). In a perfectly competitive environment, a single firm’s supply curve is the portion of the firm’s marginal cost curve that is above the firm’s average variable cost curve. That is, assuming that the price of the firm’s product is high enough so that it is more profitable for the firm to produce than to shut down (i.e., the price is greater than the firm’s average variable cost), the minimum price required to entice the firm to offer one more unit of product for sale is the cost to the firm of producing that additional unit (i.e., the marginal cost). Individual supply curves can be combined to form industry supply via the method of horizontal addition. At each price, the quantities supplied by the various firms are added to attain a single quantity supplied for the industry as a whole. When supply is represented graphically, the price is typically shown on the vertical axis and the quantity supplied is shown on the horizontal axis. Thus combining the quantities supplied of the various firms entails adding the quantities shown on the horizontal axis while holding the numbers on the vertical axis fixed. In the example below, when the price of the product is $10 per unit, Firm #1 offers 200 units and Firm #2 offers 100 units. If these are the only two firms in the industry, then the industry as a whole offers 300 units when the price is $10.

The steeper the slope of the industry supply curve, the less responsive the quantity supplied to changes in the price of the product. In the extreme case of a vertical supply curve, the quantity supplied remains fixed regardless of how high or low the price of the product might go. For example, the supply of seats at a stadium is vertical. Regardless of how high the price of tickets might go, the number of seats cannot change (at least not in the short run).

The concept of supply, and its linkage via demand to equilibria, was first formalized by the British economist Alfred Marshall (1842-1924) in his 1890 book Principles of Economics. Marshall was one of the first to conceptualize the behavior of producers and consumers independently. The approach, though common today, was not intuitively obvious. The data economists observed was equilibrium data—prices and quantities that arise only after the forces of demand and supply interact. To conceive of supply as an independent force required intuiting the existence of forces that could not be observed directly, but only inferred theoretically. Today, modern econometric techniques allow economists to obtain statistical estimates of supply and demand, but such techniques, even had they existed in 1890, would have been virtually impossible to implement without computers.

In the same way supply ignores the effect of consumers, demand ignores the effect of producers. The result is two behavioral paradigms: Supply summarizes the behavior of producers who exist (relative to consumers) in a vacuum; demand summarizes the behavior of consumers who exist (relative to producers) in a vacuum. Economists then combine demand and supply together to predict what price and quantity will result when consumers and producers are allowed to interact. The resultant price and quantity is called the equilibrium.

Bibliography:

- Eissa, Nada, and Jeffrey B. Liebman. 1996. Labor Supply Response to the Earned Income Tax Credit. Quarterly Journal of Economics 111 (2): 605–637.

- Lucas, Robert E., Jr. 1990. Supply-Side Economics: An Analytical Review. Oxford Economic Papers 42 (2): 293–316.

- Parkin, Michael. 2005. Microeconomics. 7th ed. Boston: Pearson Addison Wesley.

See also:

Free research papers are not written to satisfy your specific instructions. You can use our professional writing services to buy a custom research paper on any topic and get your high quality paper at affordable price.

ORDER HIGH QUALITY CUSTOM PAPER

Always on-time

Plagiarism-Free

100% Confidentiality

{kind=link}